Property Financial Reporting Guide for Kenyan Landlords (2026)

A 2026 guide to property financial reporting in Kenya, covering rent records, M-Pesa reconciliation, expenses, receipts, and KRA-ready summaries.

Key Takeaways

- Introduction: Why Most Landlords Fail at Financial Management

- The Real Cost of Poor Financial Management

- Understanding Property Financial Statements

- Setting Up Your Property Accounting System

Published: November 30, 2024 Updated: July 3, 2026 Reading Time: 11 minutes Keywords: Property accounting Kenya, landlord financial reporting, rental property finances, KRA tax compliance

Introduction: Why Most Landlords Fail at Financial Management

Uncomfortable truth: Many Kenyan landlords have no idea if their properties are actually profitable.

They see rent coming in and think "I'm making money." But when tax season arrives or they need a loan, they scramble to piece together months of transactions from M-Pesa statements, bank records, and crumpled receipts.

The result?

- Overpaying KRA by 20-40% (or worse, underpaying and facing penalties)

- Missing out on legitimate tax deductions

- Unable to secure financing for property expansion

- No clear picture of property performance

- Difficulty making data-driven investment decisions

This 2026 guide shows you how to set up property financial reporting around rent records, M-Pesa reconciliation, expenses, receipts, and KRA-ready summaries.

2026 refresh note: This article now separates practical bookkeeping workflows from generic accounting advice and highlights the records landlords need inside a property management system.

The Real Cost of Poor Financial Management

Enjoying this article? Get more like it.

Free landlord tips + M-Pesa rent collection guides, every 2 weeks.

Case Study: James, 8 Units in Kitengela

Before proper financial tracking:

- Thinks he's profitable ("rent is coming in!")

- No expense tracking beyond rent collection

- Files taxes based on estimates

- Can't get bank loan for expansion

- Stressful tax season every year

After implementing systems:

- Discovers actual profit margin is 45%, not "guessed" 70%

- Identifies KES 120,000 in missed deductions

- Reduces tax bill by KES 78,000 legally

- Gets bank loan approved (proper books)

- Makes decisions based on data

Annual impact: Significant savings + loan approval for expansion

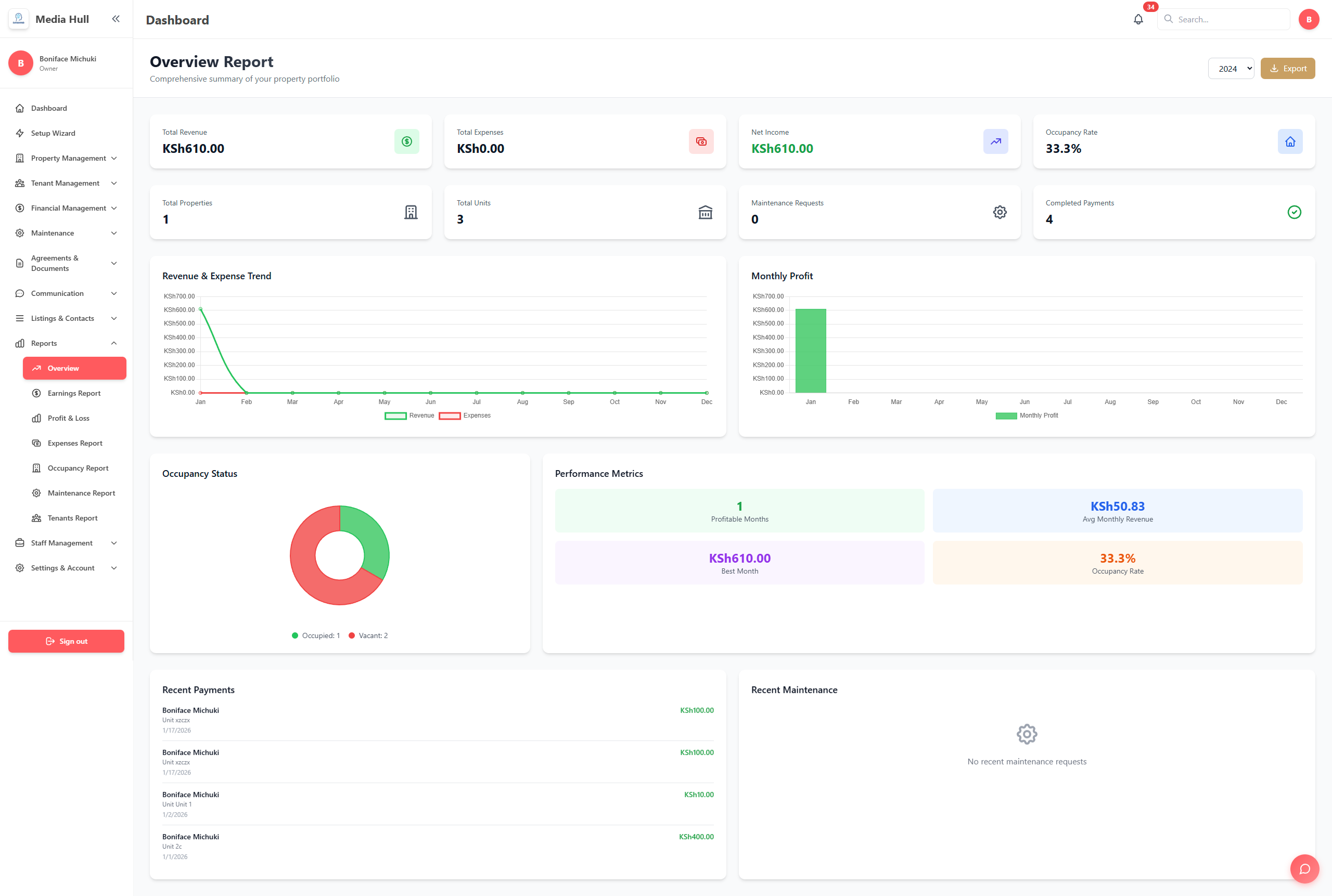

Understanding Property Financial Statements

The 3 Essential Financial Reports Every Landlord Needs

1. Income Statement (Profit & Loss)

Shows: Revenue - Expenses = Net Profit

Sample monthly income statement:

INCOME STATEMENT - JUNE 2026

ABC Apartments, Nairobi

INCOME

Rental Income KES 420,000

Late Payment Fees KES 12,000

Other Income KES 5,000

------------------------------------------

TOTAL INCOME KES 437,000

EXPENSES

Mortgage/Loan Payment KES 150,000

Property Management Fees KES 21,000

Repairs & Maintenance KES 35,000

Utilities KES 18,000

Insurance KES 8,000

Property Taxes KES 12,000

Cleaning Services KES 6,000

Security KES 15,000

Software/Tools KES 5,000

Miscellaneous KES 3,000

------------------------------------------

TOTAL EXPENSES KES 273,000

NET OPERATING INCOME KES 164,000

Profit Margin: 37.5%

What it tells you:

- Are you profitable?

- What's your profit margin?

- Where is money going?

- Which months perform best?

2. Cash Flow Statement

Shows: Money actually moving in and out

Why it matters: You can be "profitable" on paper but broke in reality.

Sample cash flow statement:

CASH FLOW STATEMENT - JUNE 2026

CASH FROM OPERATIONS

Rent Collected KES 385,000

Late Fees Collected KES 12,000

Other Income KES 5,000

Expenses Paid (KES 273,000)

------------------------------------------

NET CASH FROM OPERATIONS KES 129,000

CASH FROM INVESTING

Property Improvements (KES 80,000)

Equipment Purchase (KES 15,000)

------------------------------------------

NET CASH FROM INVESTING (KES 95,000)

CASH FROM FINANCING

Loan Received KES 0

Loan Payment (KES 150,000)

Owner Withdrawals (KES 50,000)

------------------------------------------

NET CASH FROM FINANCING (KES 200,000)

NET CASH FLOW (KES 166,000)

Opening Cash Balance KES 450,000

Closing Cash Balance KES 284,000

Key insight: Property is profitable (KES 164K) but cash decreased (KES 166K) due to loan payments and improvements.

3. Balance Sheet

Shows: Assets, Liabilities, Equity

Sample balance sheet:

BALANCE SHEET - JUNE 30, 2026

ASSETS

Current Assets:

Cash KES 284,000

Rent Receivable KES 52,000

Security Deposits Held KES 280,000

------------------------------------------

Total Current Assets KES 616,000

Fixed Assets:

Property Value KES 12,000,000

Equipment KES 150,000

Less: Depreciation (KES 300,000)

------------------------------------------

Total Fixed Assets KES 11,850,000

TOTAL ASSETS KES 12,466,000

LIABILITIES

Current Liabilities:

Accounts Payable KES 25,000

Tenant Deposits KES 280,000

------------------------------------------

Total Current Liabilities KES 305,000

Long-term Liabilities:

Mortgage/Loan KES 4,500,000

------------------------------------------

Total Liabilities KES 4,805,000

EQUITY

Owner's Investment KES 6,000,000

Retained Earnings KES 1,661,000

------------------------------------------

Total Equity KES 7,661,000

TOTAL LIABILITIES + EQUITY KES 12,466,000

What it tells you:

- Total property value

- How much you owe

- Your actual equity

- Financial health

Setting Up Your Property Accounting System

Step 1: Choose Your Accounting Method

Cash Basis Accounting

- Record income when received

- Record expenses when paid

- Simpler for small landlords

- Most common in Kenya

Accrual Basis Accounting

- Record income when earned (even if not received)

- Record expenses when incurred

- More accurate picture

- Required for larger operations

Recommendation: Cash basis for under 10 units, accrual for larger portfolios.

Step 2: Set Up Your Chart of Accounts

Income Accounts:

- 4000: Rental Income

- 4100: Late Payment Fees

- 4200: Lease Termination Fees

- 4300: Other Income

Expense Accounts:

- 5000: Mortgage/Loan Payments

- 5100: Property Management Fees

- 5200: Repairs & Maintenance

- 5300: Utilities

- 5301: Water

- 5302: Electricity (common areas)

- 5303: Internet

- 5400: Insurance

- 5500: Property Taxes

- 5600: Cleaning & Janitorial

- 5700: Security Services

- 5800: Landscaping

- 5900: Legal & Professional Fees

- 6000: Advertising & Marketing

- 6100: Office Supplies

- 6200: Software & Technology

- 6300: Bank Fees

- 6400: Depreciation

- 6500: Miscellaneous

Step 3: Implement Daily Transaction Recording

Every transaction must be recorded with:

- Date

- Amount

- Category (from chart of accounts)

- Property/Unit (if multiple)

- Description

- Payment method (M-Pesa, bank, cash)

- Receipt/Reference number

Sample transaction log:

| Date | Property | Category | Description | Amount | Method | Ref |

|---|---|---|---|---|---|---|

| Oct 1 | Kilimani Apt | Rental Income | Unit 3A Oct Rent | 35,000 | M-Pesa | RXX123 |

| Oct 3 | Kilimani Apt | Maintenance | Plumber - Unit 2B | -3,500 | Cash | - |

| Oct 5 | Kilimani Apt | Utilities | KPLC Bill Sept | -12,400 | Bank | INV890 |

Step 4: Monthly Reconciliation Process

Bank Reconciliation (monthly):

- Get bank statement

- Match all transactions in your records

- Identify discrepancies

- Add missing transactions

- Correct errors

- Verify ending balance matches

M-Pesa Reconciliation:

- Download M-Pesa statement

- Match all rent payments to tenants

- Verify amounts and dates

- Flag unmatched transactions

- Follow up on discrepancies

With proper M-Pesa integration, most payments are matched automatically.

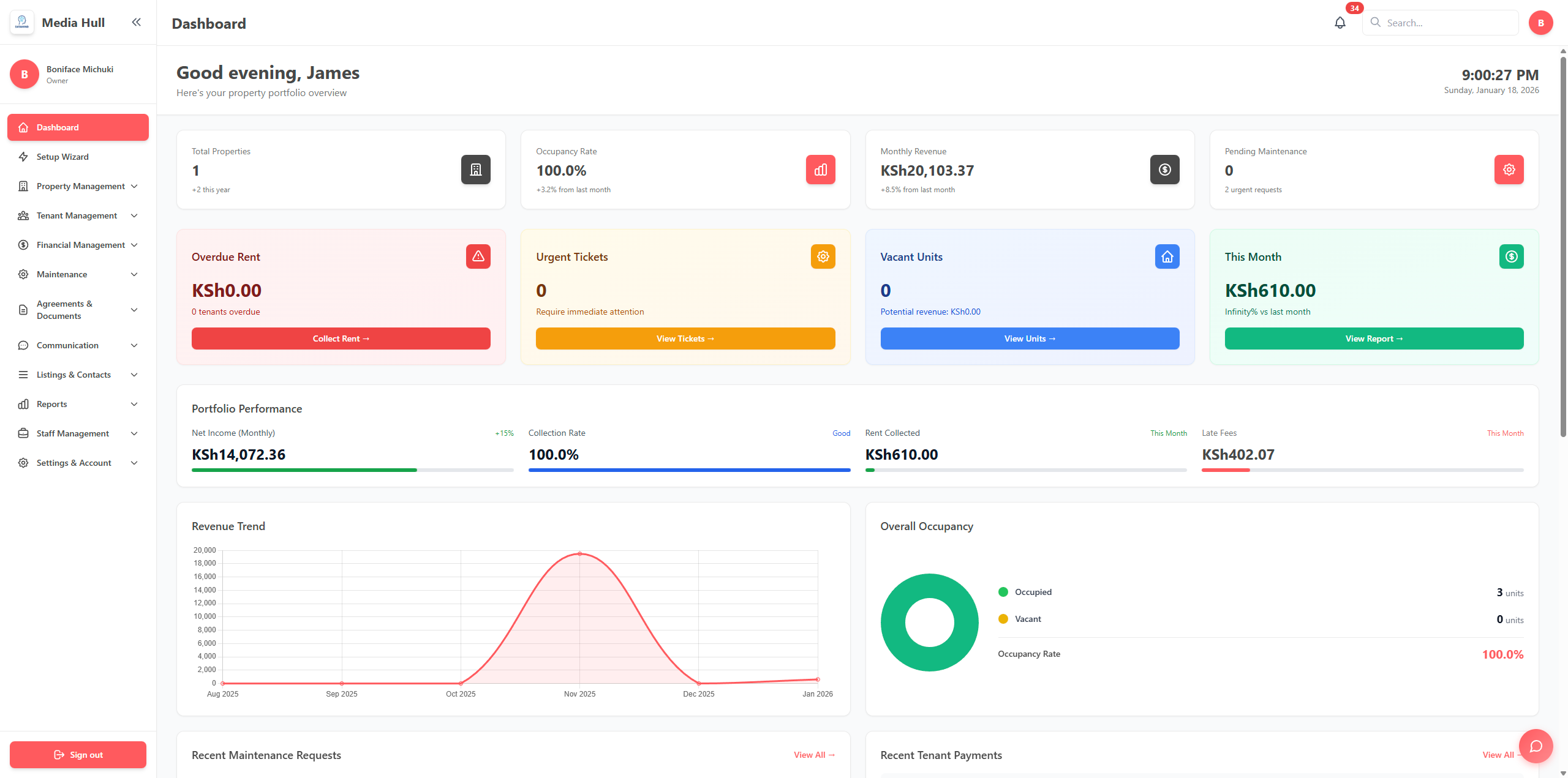

Tracking Key Performance Indicators (KPIs)

Essential Property Metrics to Monitor

1. Net Operating Income (NOI)

Formula: Total Income - Operating Expenses

Example:

- Rental Income: KES 500,000

- Operating Expenses: KES 200,000

- NOI: KES 300,000

What it shows: Property's earning power before financing

2. Cash-on-Cash Return

Formula: (Annual Cash Flow / Total Cash Invested) x 100

Example:

- Annual Cash Flow: KES 600,000

- Cash Invested: KES 3,000,000

- Cash-on-Cash Return: 20%

Benchmark: 8-12% is good in Kenya

3. Capitalization Rate (Cap Rate)

Formula: (Annual NOI / Property Value) x 100

Example:

- Annual NOI: KES 1,200,000

- Property Value: KES 10,000,000

- Cap Rate: 12%

Benchmark: 10-15% typical for Nairobi

4. Occupancy Rate

Formula: (Occupied Units / Total Units) x 100

Target: 95%+ occupancy

5. Operating Expense Ratio

Formula: (Operating Expenses / Gross Income) x 100

Example:

- Operating Expenses: KES 200,000

- Gross Income: KES 500,000

- Expense Ratio: 40%

Benchmark: 35-50% typical

6. Debt Service Coverage Ratio (DSCR)

Formula: NOI / Annual Debt Payments

Example:

- NOI: KES 1,200,000

- Annual Loan Payments: KES 800,000

- DSCR: 1.5

Requirement: Banks want 1.25+ for loans

Tax Compliance for Kenyan Landlords

Understanding Your Tax Obligations

1. Rental Income Tax

Rate: Progressive rates up to 30%

Taxable Income Calculation:

Gross Rental Income KES 600,000

Less: Allowable Deductions (KES 240,000)

------------------------------------------

Taxable Income KES 360,000

Tax Calculation:

First KES 288,000 @ 10% KES 28,800

Next KES 72,000 @ 25% KES 18,000

------------------------------------------

Total Tax Due KES 46,800

2. Allowable Tax Deductions

What you CAN deduct:

- Mortgage interest (not principal)

- Repairs and maintenance

- Property management fees

- Insurance premiums

- Property taxes and rates

- Utilities (if landlord pays)

- Cleaning and security

- Legal and professional fees

- Advertising costs

- Depreciation (4% per year)

- Bank charges and fees

- Software and tools

What you CANNOT deduct:

- Mortgage principal payments

- Property improvements (capitalize instead)

- Personal expenses

- Fines and penalties

- Owner's salary/draw

3. Residential Rental Income (RRI) Tax

Who it applies to: Landlords earning under KES 15M annually

Rate: 10% of gross rent (simplified tax)

How it works:

- Flat 10% on gross rental income

- No deductions allowed

- Simpler filing process

- May be more or less than standard rate

Example comparison:

Standard Tax:

- Gross Rent: KES 1,200,000

- Deductions: KES 480,000

- Taxable: KES 720,000

- Tax @30%: KES 144,000

RRI Tax:

- Gross Rent: KES 1,200,000

- Tax @10%: KES 120,000

Savings with RRI: KES 24,000

Note: Cannot switch mid-year, choose at start of tax year.

4. VAT on Commercial Property

When it applies:

- Commercial property rental

- Gross turnover over KES 5M

Rate: 16% on rent

Example:

- Monthly Rent: KES 100,000

- VAT @16%: KES 16,000

- Total Invoice: KES 116,000

5. Withholding Tax

Rate: 10% on rent above KES 30,000/month

Who deducts: Tenant (if corporate) or agent

What to do:

- Issue invoice

- Tenant withholds 10%

- Obtain withholding certificate

- Offset against income tax

Monthly Financial Management Checklist

Week 1: Collection & Recording

Day 1-7:

- Send rent reminders

- Receive M-Pesa payments

- Issue receipts

- Record all income

- Update tenant ledgers

- Follow up on late payments

Week 2: Expenses & Payments

Day 8-14:

- Pay monthly bills (utilities, security)

- Process vendor invoices

- Pay fundis for repairs

- Record all expenses

- File receipts/invoices

- Update expense categories

Week 3: Reconciliation

Day 15-21:

- Reconcile bank accounts

- Reconcile M-Pesa statements

- Match all transactions

- Investigate discrepancies

- Update records

- Generate draft reports

Week 4: Reporting & Planning

Day 22-30:

- Finalize monthly reports

- Review KPIs and metrics

- Analyze variances

- Plan next month budget

- Make strategic decisions

- Archive documents

Creating Professional Financial Reports

Monthly Report Template

PROPERTY FINANCIAL REPORT

Month: June 2026

Property: Kilimani Apartments

EXECUTIVE SUMMARY

- Total Income: KES 437,000 (up 5% vs Sept)

- Total Expenses: KES 273,000 (down 2% vs Sept)

- Net Profit: KES 164,000

- Profit Margin: 37.5%

- Occupancy Rate: 96% (24/25 units)

- Outstanding Rent: KES 35,000 (2 tenants)

INCOME BREAKDOWN

- Rental Income: KES 420,000 (96%)

- Late Fees: KES 12,000 (3%)

- Other: KES 5,000 (1%)

TOP EXPENSES

1. Mortgage: KES 150,000 (55%)

2. Maintenance: KES 35,000 (13%)

3. Property Management: KES 21,000 (8%)

4. Utilities: KES 18,000 (7%)

5. Security: KES 15,000 (5%)

KEY METRICS

- Cash on Cash Return (YTD): 18.5%

- Operating Expense Ratio: 28.1%

- Debt Service Coverage: 1.45

- Average Rent/Unit: KES 17,500

VARIANCES

- Maintenance up KES 12,000 (plumbing repairs)

- Utilities down KES 3,000 (water leak fixed)

NEXT MONTH PLAN

- Unit 12 renewal due (offer 5% discount)

- Schedule annual property inspection

- Budget KES 50,000 for exterior painting

ATTACHMENTS

- Detailed Income Statement

- Cash Flow Statement

- Tenant Payment Status

- Expense Details by Category

Common Financial Mistakes Landlords Make

Mistake 1: Mixing Personal and Business Finances

Problem:

- Using same bank account

- Paying personal bills from rental income

- No clear separation

Solution:

- Separate bank account for each property

- Pay yourself a set "salary"

- Keep business expenses separate

Mistake 2: Not Tracking Small Expenses

Reality: KES 500 here, KES 1,000 there = KES 50,000+ annually

Track everything:

- Hardware store purchases

- Cleaning supplies

- Transport to property

- Small repairs

- Phone calls

Tax deduction lost: KES 15,000/year by not tracking small expenses

Mistake 3: Missing Depreciation Deduction

What is it: Annual 4% property value deduction

Example:

- Property Value: KES 8,000,000

- Annual Depreciation: KES 320,000

- Tax Savings @30%: KES 96,000

Most landlords miss this!

Mistake 4: No Emergency Reserve Fund

Problem: Unexpected repairs break cash flow

Solution: 3-6 months expenses in reserve

For KES 200,000 monthly expenses:

- Minimum reserve: KES 600,000

- Ideal reserve: KES 1,200,000

Mistake 5: Forgetting Tenant Deposits are Liabilities

Wrong: Treating deposits as income

Right: Deposits are liability (owed to tenant)

Accounting:

- Receive deposit: Credit "Tenant Deposits Held"

- Return deposit: Debit "Tenant Deposits Held"

- Forfeit deposit: Credit "Other Income"

Property Financial Software vs Manual Tracking

Manual Tracking (Excel)

Pros:

- Free (if you have Excel)

- Full control

- Customizable

Cons:

- Time-consuming (10+ hours/month)

- Error-prone

- No automation

- Hard to scale

- No real-time data

- Poor multi-property support

Property Management Software

Pros:

- Automated M-Pesa tracking

- Real-time financial dashboard

- Automatic report generation

- Multi-property support

- Cloud-based (access anywhere)

- Tax-ready reports

- Audit trail

- Professional appearance

ROI Calculation:

Time saved: 10 hours/month x KES 500/hour = KES 5,000 Better tracking = tax savings: Potentially significant annually Reduced errors: Priceless

How PropFlow Simplifies Property Finances

Automated Financial Management

Income Tracking

- Auto-imports M-Pesa transactions

- Matches payments to tenants

- Generates digital receipts

- Tracks late fees automatically

Expense Management

- Records all expenses

- Categorizes automatically

- Attaches receipt photos

- Tracks by property/unit

Real-Time Reporting

- Live financial dashboard

- Income statement (P&L)

- Cash flow analysis

- Property comparison

- Trend analysis

- Custom date ranges

Tax Preparation

- Organized by tax categories

- Depreciation calculator

- KRA-compliant reports

- Rental income statement

- Deduction summary

- Export to accountant

Multi-Property Support

- Consolidated view

- Property-by-property breakdown

- Portfolio performance

- Comparative analysis

Getting Started: Your 30-Day Financial Setup Plan

Week 1: Foundation

Day 1-2:

- Open separate bank account for property

- Set up M-Pesa business number

- Organize existing financial records

Day 3-4:

- Create chart of accounts

- Choose accounting method

- Select software/system

Day 5-7:

- Enter opening balances

- Record current month transactions

- Set up tenant ledgers

Week 2: Systems

Day 8-10:

- Implement daily recording process

- Create expense filing system

- Set up digital receipt storage

Day 11-14:

- Connect M-Pesa to software

- Link bank account (if possible)

- Test transaction flow

Week 3: Reporting

Day 15-17:

- Generate first income statement

- Create cash flow report

- Build balance sheet

Day 18-21:

- Calculate key metrics

- Set financial goals

- Create budget template

Week 4: Optimization

Day 22-24:

- Review and refine system

- Train staff (if applicable)

- Create documentation

Day 25-28:

- Generate monthly report

- Analyze findings

- Make improvements

Day 29-30:

- Plan next month

- Set up recurring reminders

- Celebrate success!

Final Thoughts: Financial Clarity = Better Decisions

The difference between struggling landlords and thriving property investors isn't usually the properties themselves—it's the financial management.

With proper financial reporting you can:

- Know exactly how profitable you are

- Make data-driven investment decisions

- Maximize legal tax deductions

- Secure bank financing easily

- Identify problems early

- Plan for growth confidently

- Reduce stress during tax season

Without it:

- Flying blind financially

- Overpaying (or underpaying) KRA

- Missing expansion opportunities

- Unable to get loans

- Making emotional decisions

- Constant financial stress

Start Your Financial Transformation Today

PropFlow provides everything you need for professional property financial management:

- Automated M-Pesa income tracking

- Expense management with receipt storage

- Real-time financial dashboard

- One-click financial reports

- Tax-ready documentation

- Multi-property consolidation

- KPI tracking and analytics

Pricing:

| Plan | Price | Properties |

|---|---|---|

| Starter | KES 2,999/month | Up to 3 |

| Professional | KES 7,999/month | Up to 10 |

| Enterprise | KES 19,999/month | Unlimited |

Setup: Under 10 minutes Free Trial: 2 months, no credit card required

About PropFlow

PropFlow is a property management platform built specifically for Kenyan landlords. We combine M-Pesa integration with comprehensive financial management tools to give you complete visibility into your property business.

Website: propflow.ke WhatsApp: 0701 822 032 Email: hello@propflow.ke

Related Articles:

- Automated Property Management in Kenya: 2026 Landlord Guide

- M-Pesa Rent Collection: Complete Guide for Kenyan Landlords

- Tenant Management Best Practices for Kenyan Landlords

Share this guide with landlords who want better financial control and lower taxes.

Get Free Landlord Tips in Your Inbox

Join 500+ Kenyan property owners. Get M-Pesa collection tips, tenant management guides, and PropFlow updates every 2 weeks.

No spam. Unsubscribe anytime. We respect your inbox.

Related Articles

Keep reading

Best Property Management Software in Kenya for Landlords in 2026

A detailed 2026 guide to choosing property management software in Kenya, covering M-Pesa rent collection, tenant records, maintenance, reports, KRA-ready records, and PropFlow.

How Much Kenyan Landlords Actually Lose to Late Rent (and 5 Ways to Fix It)

The real KES cost of late rent in Kenya, with a 12-unit Nairobi example and 5 fixes that drop late-payment rates from 20% to under 4%.

Spreadsheets vs. Property Management Software in Kenya: A KES Cost Breakdown (2026)

A shilling-denominated comparison of running rentals on Excel vs. a proper property management system. Includes a 10-unit case study.